RDSP Example:

Last November, I did a RDSP workshop for families with special needs. During the presentation, I illustrated an example of how contributions toward the Registered Disability Savings Plan could bring in huge benefits from the government. Many attendees were astonished after we went through the calculations together. Below is an example I recently read from an article on Advisor.ca, written by Carol Bezaire, the vice-president of tax and estate planning at Mackenzie Investments.

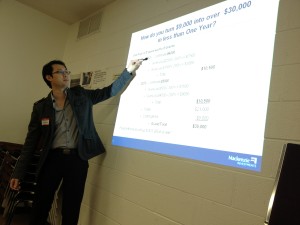

If you could recall, the government of Canada will match 300% for the first $500 in contributions each year, while 200% for the next $1,000. Although the lifetime contribution limit is $200,000, the maximum CDSG paid to the RDSP in any given is $10,500. Since unused contribution rooms can be carried forward, a qualified beneficiary who setup a new RDSP in 2013 can make up the contributions all the way back to 2008 (Given that the beneficiary was already eligible for DTC). Here’s the strategy where one uses the RDSP to turn $12,000 of disability savings into $40,000 in three years.

First Year – 2013

A contribution of $3,750 will attract $10,500 in Canada Disability Savings Grant (CDSG) as follows:

6 years (From 2008 to 2013 inclusive, due to carry forward) x $500 x 300% = $9,000

0.75 years* x $1,000 x 200% = $1,500

Total: $10,500

*What is the 0.75 Years? Remember, there is a ceiling of $10,500. In order to receive $1,500 in government matching, you just need to use up 0.75 years of the $1,000-per-year carry forward, leaving you with 5.25 years (6 – 0.75) to use in 2014.

Second Year – 2014

A contribution of $5,000 will generate another $10,500 in disability savings grants:

1 year (2014) x $500 x 300% = $1,500

4.5 years** x $1,000 x 200% = $9,000

Total: $10,500

**What is the 4.5 Years? You now have 6.25 years’ worth of $1,000-per-year carry forward.Since there is a cap, to trigger $9,000 in CDSG, you just need to use 4.5 years of that carry forward, with the remainder of 1.75 years (6.25 – 4.5) to use in 2015.

Third Year – 2015

A contribution of $3,250 will bring in $7,000 in CDSG. After this deposit, all the unused contribution room will be used up and the matching grants from 2008 to 2015 will be received.

1 year x $500 x 300% = $1,500

2.75 years * x $1,000 x 200% = $5,500

Total: $7,000

* What is the 2.75 Years? The remaining $1,000-per-year carry forward, 1.75 plus the 2015 $1,000-per-year matching

As you could see, with contributions ($3,750+$5,000+$3,250=$12,000), it will trigger ($10,500+$10,500+7,000=$28,000) Canada Disability Savings Grants. This is how one could turn $12,000 disability savings into $40,000 in 3 years. Furthermore, this has not even include any investment growth and the Canada Disability Savings Bonds. Lower income beneficiaries can benefit from a carry forward of CDSB of $1,000 per year, to a maximum amount of $11,000 in any given year. Once again, the carry forward amount can go as far back as 2008, up to 10 years or date of diagnosis, whichever is most recent. Contributions to the RDSP are not required to be eligible for CDSB.

To find out how much government grants you could receive, feel free to contact me.