Two weeks ago, I sent out a reminder to the families that I’m working with to start planning for their RDSP contribution in 2017. Especially, by the month of March, many of them have already received their “Annual Statement Of Grants Entitlement for 2017”. This is the letter which stated how much should their family contribute into their RDSP, in order to receive the maximum amount of Canada Disability Savings Grants.

I recently received an inquiry from a client, and she asked: “Sam, I understand that the RDSP could be very helpful to families with special needs, but can you show us an illustration of the benefits in savings within this account?”

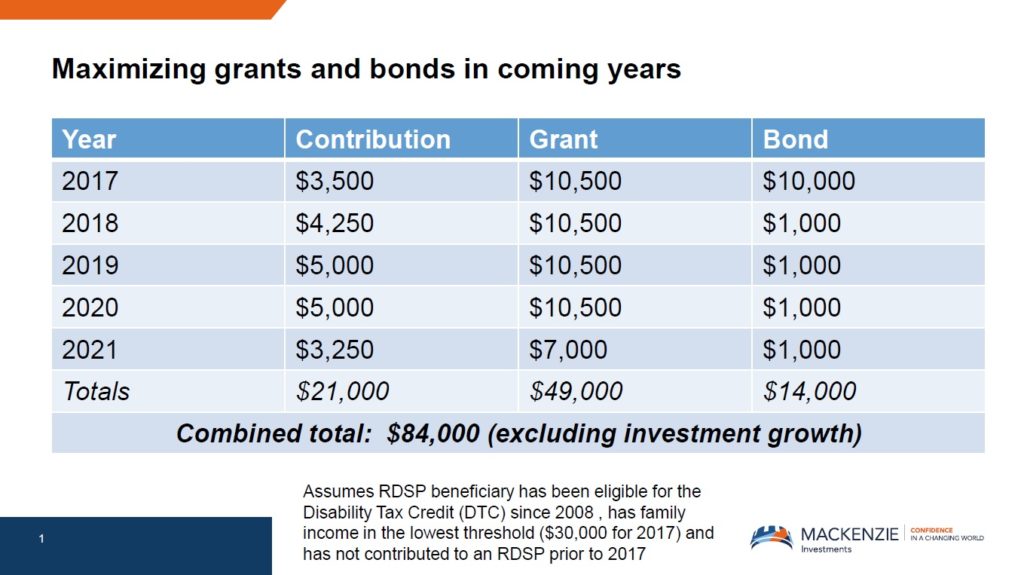

Yet, sometimes, a numeric example could illustrate the point a lot better than an abstract concept. Earlier in 2017, I had a discussion with the Mackenzie’s Tax and Estate team, and below is the illustration I received from them. Before we jump into reviewing the figures, it’s important to understand there are several assumptions in this example.

Danielle is a young girl with autism, she has been diagnosed with this condition by her doctor in the year 2008. Her physician helped her family to complete the T2201 form, and her disability tax credit was also approved by the CRA on the same year. Danielle is the only daughter of her parents, and also living together with them. Danielle’s mother needs to spend a lot of time taking care of her daily activities, therefore, her father is the only income earner. Hence throughout all the years, their family incomes are always lower than the first threshold on the CDSB table (Click here to view the 2017 RDSP Income Matching Rates)

In year 2017, an RDSP account is setup, with both her parents as the account holders, and Danielle as the beneficiary. To catch up the carried grants from the previous years, her parents did the following:

In the above example, Danielle’s parents redirect $21,000 of their savings, which leads to $49,000 of “Canada Disability Savings Grants”. But the benefits do not just stop there, because there is also the “Canada Disability Savings Bonds“. This bond provides extra benefit to low-income family, with up to $1000/year. In this example, from the year 2017 to 2021, government would deposit another $14,000 into their RDSP account, which boost the RDSP account total balance to be $21000+49000+14000= $84,000

Rather than leaving the money in a regular savings account, which generate very little interest these days, Danielle’s parents have successfully turned their savings of $21,000 into $84,000 in 5 years, which is a great milestone in building up the long-term savings for Danielle.

Want more updates regarding the RDSP? Click here to subscribe to my e-newsletter.

- Disclaimer: The above figures are obtained from Mackenize Investments, only for illustration purposes, and not intend to provide specific financial advice. The amount of government grants and bonds one could receive depends on many factors such as the eligibility of the disability tax credit, family net income, age, therefore, they could be differed for each individual’s case. Market conditions, tax laws, and investment factors are subject to change. Individual should always consult with a financial professional before making any decision